Commentary – 2021 4th Quarter

10/21/2021

The four most expensive words in the English language are, “This time it’s different.”

- Sir John Templeton

Follow The Money

In psychology, there is a phenomenon known as The Paradox of Choice. Essentially, it stipulates that an abundance of options can, somewhat counterintuitively, decrease our satisfaction. If you only had to choose between 1% and 2% milk, you can easily weigh the pros and cons and be confident in your decision. Of course, there is also skim milk and whole milk. There are gallons and half-gallons. Nowadays, there are milk alternatives, designations about how the milk was sourced, and milk formulas for sensitive stomachs. In short, more choices translate to an increasingly difficult task of knowing what is best.

Writing our commentary this quarter feels a bit like standing in the milk aisle. There are several topics and trends demanding attention in the current economy and financial markets. It is somewhat paralyzing to know which one to follow, which one to write about, which one is an indicator, and which one is a red herring. In an interconnected global economy, the right answer may be quite simple; all of them are important.

So, in the interest of transparency, these are the five major market conditions and trends we are monitoring as 2021 draws to a close:

- Monetary easing has created an immense surge in wealth

- The economic drag from COVID-19 is beginning to wane

- Inflation is here to stay

- The Federal Reserve is tapering and will begin tightening in 2022

- Fiscal policy will be much less accommodative in 2022

There is no shortage of headline material, but there is a disturbing lack of narrative. The Federal Reserve, brimming with unearned confidence, injected unprecedented liquidity into the marketplace to fight the anticipated economic effects of COVID-19. 18 months later we are faced with an eerie feeling of, “okay, now what?” Or perhaps a more ominous feeling of, “was it too much?” This seems to be the consensus, as bearish sentiment over the last year recently peaked on September 29th[1].

We are less pessimistic. While unwinding cheap money policies will prove difficult, there is nothing to suggest that it will send markets into a recessionary tailspin. This is usually characterized by irresponsible debt-use. Luckily, the surge in wealth has come in large part from the debt side of consumer’s balance sheets. This appears to be the case for the ultra-wealthy all the way through lower middle-income households. Household debt-service ratio (debt payments as a percent of income) is at a 40-year low[2].

Furthermore, the Centers for Disease Control is estimating that close to 90% of Americans are either vaccinated, have been infected, or both, suggesting that the worst of the COVID-19 pandemic is behind us. This of course does not consider variants, but recent data also from the CDC is showing that the Delta wave has likely crested. While “it ain’t over ‘til it’s over,” these are encouraging signs that the economy should no longer need assistance to stay afloat. This means a job market which can hopefully return to normal. We have seen the highest wage growth since the 1980s with a 5% increase year-over-year. This is good news for an economy searching for the next driver of growth.

Of course, high wage growth and a tight labor market are not without consequences. As we wrote last quarter, inflation has been a major economic byproduct of the pandemic. The potential of runaway inflation (a la the 1970s) is a theory that has picked up steam recently. There are two reasons this is highly unlikely. The first is a measurement called “trimmed-mean personal consumption expenditures,” which is a fancy title for a rather simple calculation—the inflation rate minus whatever good or service had the largest swing. It makes a big difference in environments like today. For example, in June, July, and August the headline Consumer Price Index was up 5.4%, but the trimmed version was at only 2%[3].

The difference is simply removing the huge increase in automobile prices. This came from chip shortages caused by supply chain issues, which is the second reason that runaway inflation is unlikely. Supply chain tends to be a transitory contributor to inflation. It comes in like a lion but goes out like a lamb. If history is any guide, corporations will adapt.

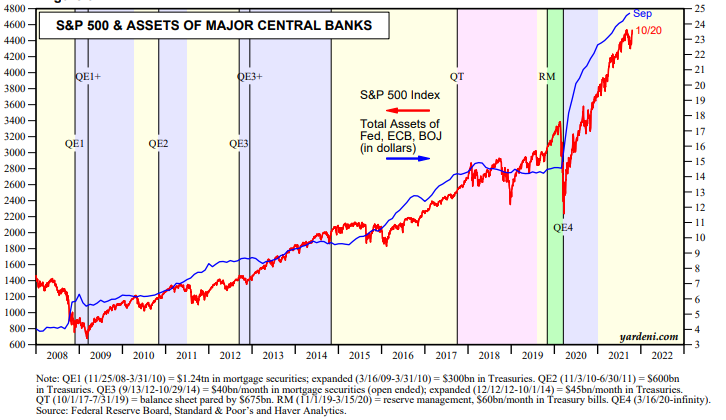

Perhaps the item with the most direct impact on financial markets will be how the Federal Reserve decides to combat sustained inflation. The Fed’s role as “lender of last resort” has been transformed into “ultimate market maker.” This has been exacerbated by the pandemic as half of the Fed’s $8.5 trillion balance sheet was from liquidity created over the last 18 months. It had been buying $120 billion of bonds on the open market (i.e., injecting cash) every month up until September. It is no wonder that the market ended the third quarter on a slide—the process of tapering has begun.

Tapering essentially means that the Fed is slowing their process of creating extra cash, but not stopping it. The plan is to reduce bond purchases by $15 billion every month until they are no longer creating extra liquidity. Simple math says this will take 8 months to come to fruition, teeing up the potential for interest rate hikes as early as next summer. This is when tapering can turn to tightening and a stock market accustomed to cheap capital can diverge from an otherwise healthy economy.

Coupled with the rapid increase in inflation, this is particularly bad news for technology and growth stocks. Since many major indexes are weighted by market capitalization, it can also threaten the overall stock market. The “stocks are overvalued” narrative may have more credence in 2022 than it has in prior years, but we do not believe the threat of a correction to be anything more than a temporary pull back. The last time the Federal Reserve started tightening was late 2017. The S&P 500 was flat for almost a year, then went on to an abrupt three-month correction. It bottomed out on Christmas Eve 2018, down 19.4% off the peak (see the pink-shaded section labeled “QT” below).

It then came roaring back, without further monetary easing, up until the dawn of the COVID pandemic. This was obviously met with ferocious cheap money policies and equity markets followed the trend.

While correlation does not necessarily mean causation, the long-term nature of this trend appears to lend it credibility. The last time there was tightening, stocks were choppy, there was a pullback, and ultimately a recovery; all within 18 months.

We expect history to repeat itself.

Tax Change De-Bunking

Heading into 2022, tighter fiscal policy appears to be on the horizon. Tax law changes are intended to stoke a feeling of urgency. After all, it is a revenue generating activity for the federal government. In our experience, the messaging is ultimately very successful—many individuals feel compelled to do something about tax changes. This should not be a foregone conclusion.

The American Families Plan is proposed legislation which makes some tweaks to the current tax brackets and reverses some changes of the Tax Cuts and Jobs Act (also known as the “Trump tax cuts”) which was put into place in 2017. It also extends some provision of the American Rescue Plan Act (also known as the “COVID bailout”).

Normally, we do not like to make any formal comment on speculative or proposed tax reforms. It is very rare for new legislation to be put in place without advance notice. Furthermore, it is difficult to make recommendations based on conjecture. Until the new law is known, implementation is likely ill-advised.

While this time is no different, the American Families Plan appears to have some provisions with bipartisan support. Here are the key items which deserve consideration[4] –

- Make permanent the Child Tax Credit from the COVID rescue plan: families will continue to receive a tax credit for $3,000 per child for children six years and older ($3,600 per child under six) which is fully refundable. It will be delivered to families throughout the year as a prepayment of the credit.

- Make permanent the Dependent Care Credit from the COVID rescue plan: families will continue to receive a tax credit for half of their spending on child care for children under age 13 up to a maximum of $4,000 per child or $8,000 for two or more children (phased out for families making $125,000 or more up to $400,000).

- Change the Top Tax Bracket: increase the top tax rate from 37% to 39.6% for income over $400,000 for single filers (currently $523,600) and $450,000 for married filing jointly (currently $628,300).

- Change the Capital Gains Tax: increase the capital gains tax rate for households making more than $400,000 for single filer and $450,000 for married filing jointly. Instead of paying the lower, preferential tax rates on long-term capital gains and qualified dividend income (currently 20%), such income will be subject to ordinary income tax rates of up to 25%.

- Eliminate Roth Conversions: the top tax bracket would not be allowed to convert IRA dollars to Roth IRA after December 31, 2031. Effective immediately, after-tax amounts in IRA will not be allowed to be converted to Roth, which would eliminate the “backdoor Roth” strategy.

There are three items notably missing from the draft legislation. Two are both hot topics relating to capital gains: the elimination of like-kind exchanges for real estate to defer capital gains tax, as well as the elimination of the step-up in cost basis at death. It appears that these two strategies will remain intact. The third is removing the $10,000 limitation of deducting property taxes (the SALT provision), which will likely stay in place.

There are several other esoteric changes, which all essentially boil down to this: if you make more than $450,000, you are considered high-income. These taxpayers will now be subject to a slew of different rules than those under the same threshold.

From a planning perspective, it is also important to note that the current tax brackets (as well as some provisions) are set to revert to pre-2017 levels as of January 1, 2026, unless new legislation is passed. In other words, there will be a 4-year window to implement tax strategies once the new legislation is passed before Congress goes back to the drawing board.

From Bytes to Bits

The internet has mostly fulfilled the prophecies made during its inception. At the time, it was mostly advertised as an information highway (as seen on a TIME Magazine cover), bringing news, communications, and entertainment to your fingertips. It promised to revolutionize everything from shopping habits to data storage, and even our personal relationships.

While it feels that almost every aspect of our lives has been exponentially altered by technology, there is one notably missing—how we manage our money. Sure, balancing a checkbook by hand is nowadays a foreign concept, mostly due to online banking portals, budgeting software, and similar tools. Writing checks by hand is less commonplace with automatic payments. Physical stock certificates are no longer issued due to financial firms’ ability to report data.

The internet was technically invented in 1983. It has gone through multiple iterations and upgrades, paving way to the current era of internet technology. The same cannot be said about the two major electronic systems used for financial transactions –

- The ACH (Automated Clearing House) System: first used in 1972 to replace paper checks and transfer cash between accounts and institutions

- The ACAT (Automated Customer Account Transfer) System: first used in 1985 to replace the paper stock certificates and standardize the transfer of investment assets between custodians

Ever wonder why, in today’s paperless, electronic world, that you cannot transfer cash on a weekend? Why would “the internet” observe bank holidays?

The answer is quite simple—these systems have not been re-engineered since before the internet was invented and the financial institution is still required to physically intervene in every transaction. It is likely by design that the world of finance has been absent from the technological revolution, as this verification of trust is what makes the banks viable and, therefore, able to charge fees.

It is no wonder that this has led to a groundswell of support for a broader use of cryptocurrency. On this, there are competing schools of thought. The naysayers point to the earliest adopters of the technology as examples of its potential for nefarious use for cyberhackers, drug dealers, and money launderers alike. The DeFi (Decentralized Finance) advocates are on the exact opposite side of the spectrum—they believe that the “imperfect, yet pure” nature of a truly decentralized currency has benefits which outweigh the detriments.

No matter which side of the fence you fall on, or somewhere in the middle, the move towards cryptocurrency is no longer an issue that can be ignored. The blockchain technology behind it has more applications than currency alone. This is very likely to be a big disrupter; the “next internet,” if you will.

There are two reasons that we think blockchain and cryptocurrency may soon see it’s time in the limelight. China’s move towards a state-backed cryptocurrency is substantial. One of the main detractors of using a decentralized currency is that there is no government backing. Enthusiasts are quick to point out that currency is paper which is only worth what we decide it is worth as a society, but it will be difficult to put more faith into a faceless network of computers than federal governments. Utilizing the technology, while solving the government backing problem, is an inventive solution.

The second reason, and perhaps the most eye-opening, is simply how large the technology is starting to become even without any oversight. Bitcoin is still the best-known cryptocurrency, potentially because it was the first, but this has gone through multiple iterations while the banking system remained stagnant. Today, Ethereum is a blockchain technology which verifies most of the cryptocurrency transactions. Consider the point-of-sale terminal where you swipe your credit card, then Visa verifies the transaction. In Q2 2021, Visa verified $2.5 trillion of transactions. Ethereum verified the same amount[5]. In other words, there is as much money changing hands using cryptocurrency as there is using Visa cards.

We hope you enjoyed our comments. If you have any questions, please do not hesitate to contact us. We welcome the opportunity to discuss our thoughts in greater detail. Thank you for your continued confidence in Planning Capital.

Sincerely,

The Planning Capital Team

Author

Daniel B. Brady, MBA, CFP® │ Partner

Contributors

Richard W. Bell, Jr., CKA® │ Partner

David A. Emery, MBA, CFP® │ Senior Financial Planner

Jay D. Ahlbeck, CLU®, ChFC® │ Senior Financial Planner

Paul C. McClatchy, MBA, CFP® │ Senior Financial Planner

Jeffrey A. Sprowles, CFP® │ Senior Financial Planner

[1] AAII Investor Sentiment Survey, September 29, 2021

[2] FactSet, J.P. Morgan Asset Management, U.S. Guide to the Markets, September 30, 2021

[3] “Fighting Trim,” The Economist, September 18, 2021

[4] Jeffrey Levine, “Tax Changes Proposed in the American Families Plan,” Horsesmouth, September 23, 2021

[5] “Down the Rabbit Hole,” The Economist, September 18, 2021